Don’t just meet your customers’ expectations—exceed them!

In this article, we delve into why customer retention is both economically sensible as well as crucial for long-term success in the insurance sector. We’ll examine the costs associated with customer acquisition and the profound impact of the claims process on customer loyalty.

Don’t miss the subsequent parts of the series, where we’ll explore in-depth the pivotal role of the claims experience in retention and how Experience.com provides an innovative solution for revolutionizing this journey.

The Competitive Landscape

The insurance market today is a battlefield of competitiveness.

Companies grapple not just with one another but also with the escalating costs of acquiring new customers.

In an industry where captive insurers like State Farm and Allstate expend an average of $792 in customer acquisition costs — a figure that climbs to an average of $900 with the inclusion of independent agents — the emphasis on customer retention becomes not just a strategic advantage, but a survival imperative.

With such high stakes, it’s essential to understand the economics of customer acquisition and retention and identify pivotal moments in the customer journey — none more critical than the claims process.

The Economics of Customer Acquisition

The pathway to acquiring a new customer in the insurance industry is not only competitive but expensive. Investments are poured into marketing campaigns, agent commissions, competitive pricing strategies, and more. The cost disparity becomes even more evident when comparing captive insurers with independent agents, with the latter incurring higher costs due to their broader, more personalized scope of service. These expenses underscore a critical realization: customer acquisition, while necessary, is not a sustainable standalone strategy for growth and profitability due to its high cost and uncertain returns.

Adding to this, the average cost per claim, a critical KPI, further complicates the picture.

Verisk Analytics reports the average auto collision claim to be $3,160, and the Insurance Research Council cites the average homeowner’s insurance claim as $626.

These figures are crucial for insurers, highlighting the need to balance policy pricing with the risks associated with each policy type.

The Value of Customer Retention

Contrasting the high costs of acquisition, customer retention emerges as a more economically sound strategy. Retained customers provide a consistent revenue stream, are more likely to purchase additional policies, and often become brand advocates, referring new customers at no additional cost. The financial benefits of customer retention are underscored by studies showing that $1 invested in customer retention results in more than $5 in profits compared to new customer acquisition.

Furthermore, the importance of metrics like loss ratio, which stands at an average of 55.2% across all insurance lines according to the National Association of Insurance Commissioners, cannot be overstated. This ratio is a health indicator for insurance companies, reflecting whether they are collecting adequate premiums to cover claims. A high loss ratio can signal financial instability, making customer retention even more critical for maintaining a healthy income statement. Retention can help overall profitability but another critical metric Experience.com closely impacts is Combined Ratio, just like Loss Ratio this includes the cost of handling the claims. And because we can help identify issues with claims processes, we can help reduce the cost of claims administration.

Identifying the Moment of Truth: The Claims Process

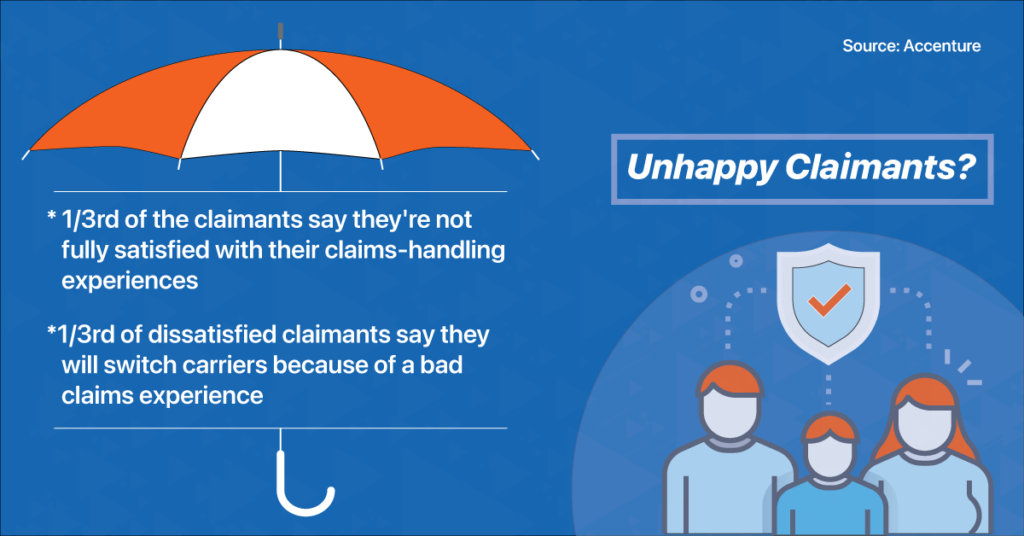

The claims process is often the defining moment in the insurer-customer relationship. It’s the touchpoint where policies and customer service are put to the ultimate test. Metrics such as the average time to settle a claim become vital in this phase. As per J.D. Power & Associates, claim cycle time significantly influences customer satisfaction, with the shortest average cycle reported at 11 days.

But it’s not just about speed; it’s also about the quality of service. Claims frequency varies with the type of insurance — high for workers compensation and auto collision, moderate for general liability, and low for property losses, as stated by the International Risk Management Institute. Each requires a tailored approach, ensuring customers feel supported and valued, significantly impacting renewal rates. In fact, an efficient, empathetic claims process can boost retention rates, which hover around 84% industry-wide as per The Independent Insurance Agents of Dallas.

In Conclusion

The contemporary insurance landscape underscores the critical importance of customer retention, given the high costs and complex dynamics of customer acquisition. The claims process stands out as a critical juncture in determining customer loyalty. By focusing on enhancing this experience — through speed, efficiency, and empathy — insurers can significantly improve their retention rates, ensuring sustainable growth and profitability. As we advance into the next article, we will unravel the complexities of the claims experience in more detail, showcasing strategies to optimize this pivotal touchpoint for improved customer retention.

Click here to navigate to Article 2: The Pivotal Role of the Claims Experience in Customer Retention

Ready to transform your customer’s claims journey experience and improve retention rates significantly?

Take the first step today!

Book a Demo with Experience.com and see firsthand how our solutions can revolutionize your approach to customer experience in the insurance claims process.

Don’t just meet your customers’ expectations—exceed them!